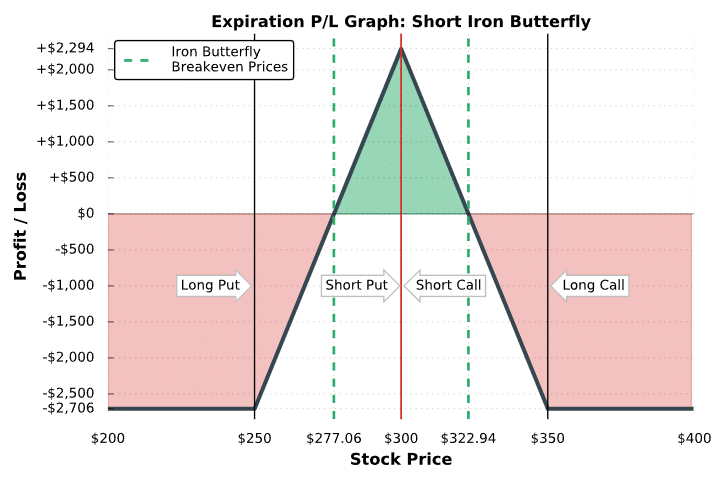

As illustrated above, the short iron butterfly strategy realizes its maximum profit potential when the stock price is trading at the short strike at expiration, which has a low probability of occurring. However, since the short iron butterfly can collect a lot of premium, making partial profits on a short iron butterfly still results in healthy profits compared to making full profit on strategies that collect less premium (such as a short strangle).

Additionally, you’ll notice that a short iron butterfly has a similar risk profile to a short straddle, except the risk of a short iron butterfly is limited beyond the long options.

Regarding loss potential, both the short call spread and put spread are $50 wide. Because of this, the maximum potential loss is: ($50 strike width – $22.94 credit received) x 100 = $2,706. However, if the call spread were $75 wide (e.g. 300 short call and 375 long call), the maximum loss potential of this iron fly would be: ($75 strike width – $22.94 credit received) x 100 = $5,206. So, the loss potential of a short iron fly always depends on the width of the wider spread.

When each spread has the same width, the risk of loss is equal on both sides.

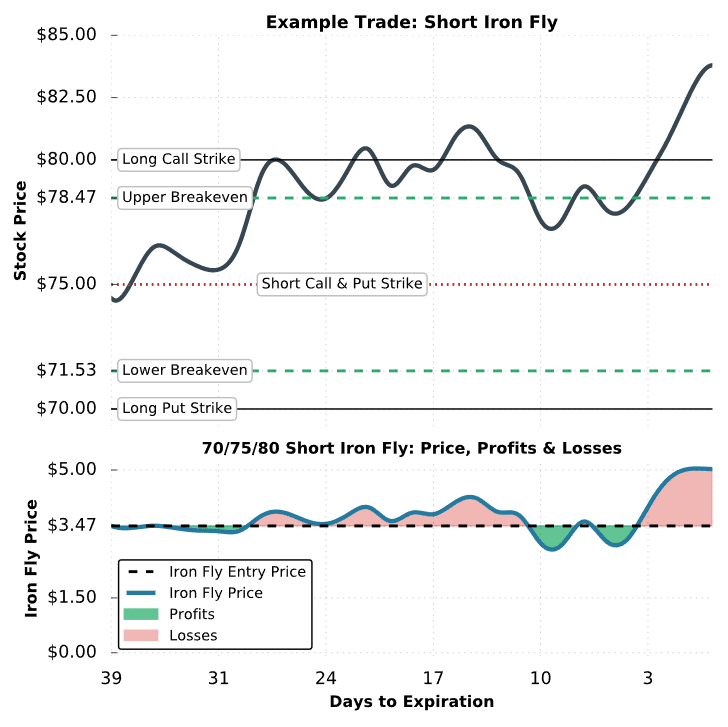

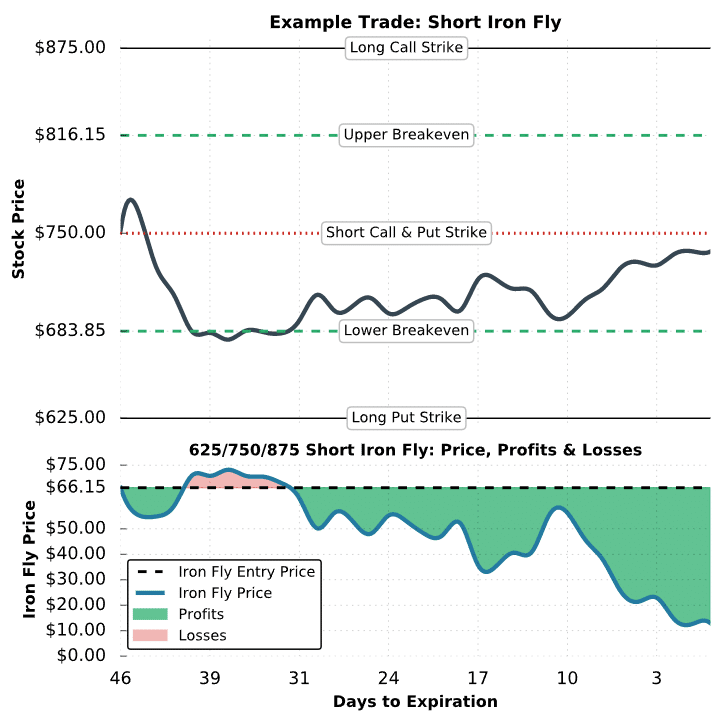

Nice job! You’ve learned the general characteristics of the short iron fly strategy. Now, let’s go through some visual trade examples to solidify your knowledge of how selling an iron butterfly works in practice.

Wow! This blog looks just like my old one! It’s on a totally different topic but it has pretty much the same page layout and design. Great choice of colors!