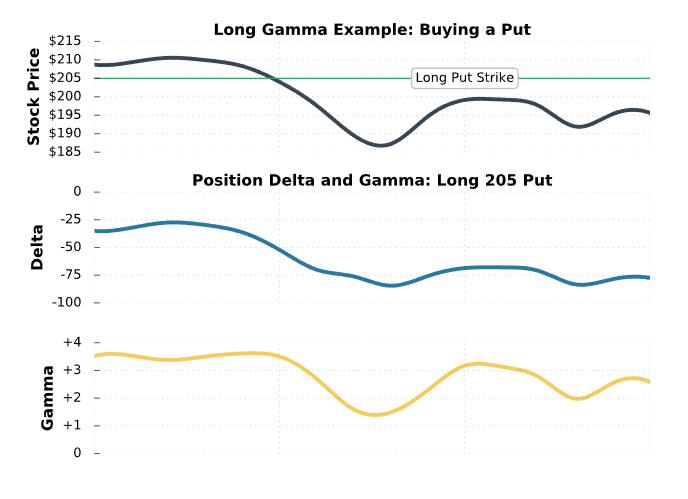

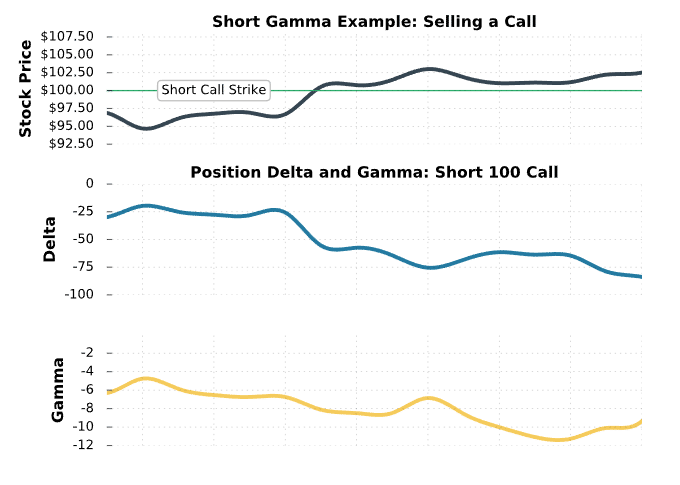

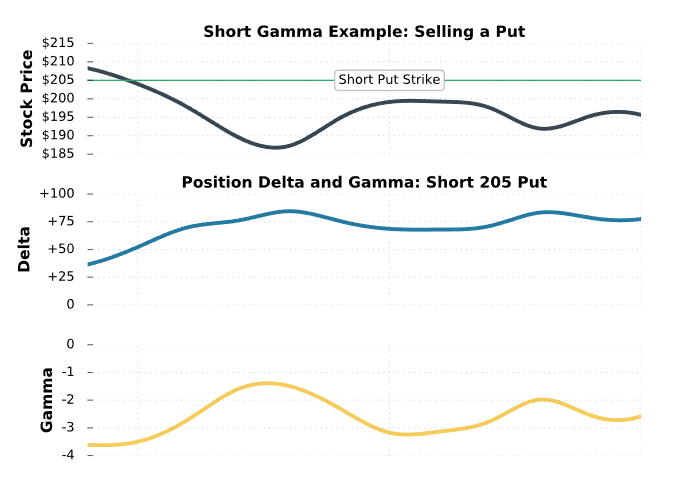

“Gamma scalping” is when an options trader buys/sells shares of underlying stock against a long/short option position.

The goal is to periodically adjust the position’s delta by trading in and out of underlying stock with the intention of profiting from the overall stock/option position.

Profits can stem from the share trading activities, or the option position value changes.

For example, a gamma scalper who shorts a straddle will need to buy stock as the share price increases and sell stock as the share price falls. The trader will profit from the strategy if the stock volatility is low, driving profits from the short straddle decay with minimal losses from the stock trading.

Conversely, a gamma scalper who buys a straddle will need to short stock as the share price increases and buy stock as the share price falls. The trader will profit from the strategy if the stock volatility is high, driving profits from the stock trading activities that exceed losses from the long straddle’s decay.

Gamma scalping is also known as “dynamic delta hedging,” and is an active trading strategy used by extremely sophisticated traders.

(1)")

One thought on “Long Gamma and Short Gamma Explained (Best Guide)”

The charts are very helpful to the readers they can easily understand it. Great.