Search

Search

About

Blog

Contact

Menu

About

Blog

Contact

Search

Search

Watch on YouTube

Category: Options Trading

tastytrade Analysis Tab (Trading Platform Tutorial)

Read More »

March 28, 2025

tastytrade Positions Tab (Trading Platform Tutorial)

Read More »

March 28, 2025

tastytrade Trade Tab (Ultimate Trading Platform Tutorial)

Read More »

March 28, 2025

Why Trade With tastytrade? (Ultimate Platform Overview)

Read More »

March 28, 2025

Options Trading

Implied Volatility Guides (with Visual Examples)

Read More »

May 22, 2025

Options Trading

IV Rank vs. IV Percentile: Which is Better?

Read More »

April 14, 2022

Options Trading

VIX Term Structure – The Ultimate Guide w/ Visuals

Read More »

March 16, 2022

Options Trading

Trading VIX Futures | Options Volatility Guide w/ Visuals

Read More »

March 14, 2022

Options Trading

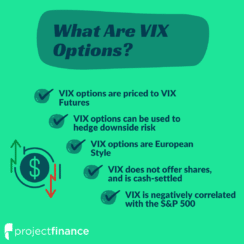

Here’s How to Trade VIX Options (3 Things to Know)

Read More »

May 3, 2022

Options Trading

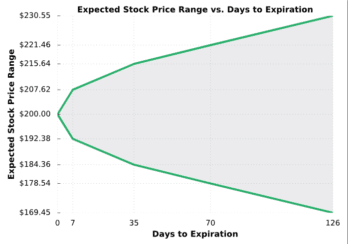

Expected Move Explained: Options Trading

Read More »

September 4, 2024

«

Page

1

Page

2

Page

3

Page

4

Page

5

»