Category: Investing

Leverage 101: Borrowing Money to Buy Assets

How do the wealthy use the above information?

“Buy, borrow, die.” is how.

What the saying means is that you buy assets with your earnings over time, borrow against them to avoid capital gains and continue holding appreciating assets, then die. It’s a cheeky way of saying you’ll never sell the assets you accumulate.

The idea is to avoid selling assets at all costs because holding assets long-term protects you from inflation, eliminates capital gains taxes, and prevents interrupting long-term compounding.

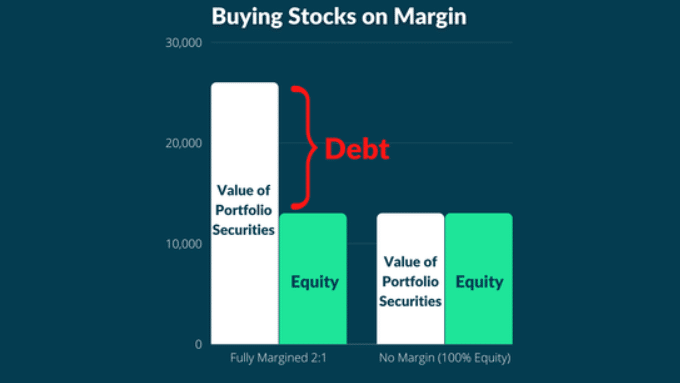

If you can borrow against your assets at an interest rate lower than the long-term annual growth rate of the assets, you come out ahead.

A WSJ article quoted a 3.2% interest rate on asset-backed loans from Merrill Lynch for those with $1M+ in assets, or 0.87% for those with $100M+ in assets:

|

I ran a basic simulation of a stock portfolio worth $1M compounding at 8% per year. I compared selling 25% of the portfolio to come up with $250K in cash vs. borrowing $250K at 3.2% interest for 10 years.

The BankRate Amortization Calculator showed a $2,450 monthly payment for that loan with a total interest cost of $42,500 over the 10 years:

Of course, this means you’ll be selling your asset during a downturn, which is likely when you’d want to be acquiring more of that asset.

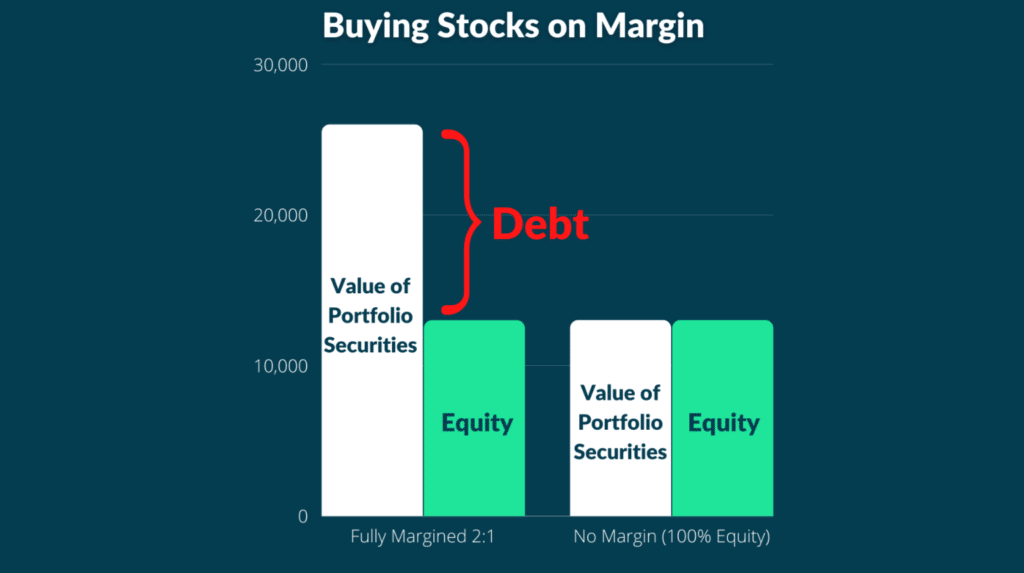

So the benefit of taking out an unsecured personal loan to buy an asset like a portfolio of stocks or bitcoin is that you won’t be forced to sell those assets if their values fall.

So as long as you can keep the bank happy by continuing to make the loan payments, you’ll be just fine.

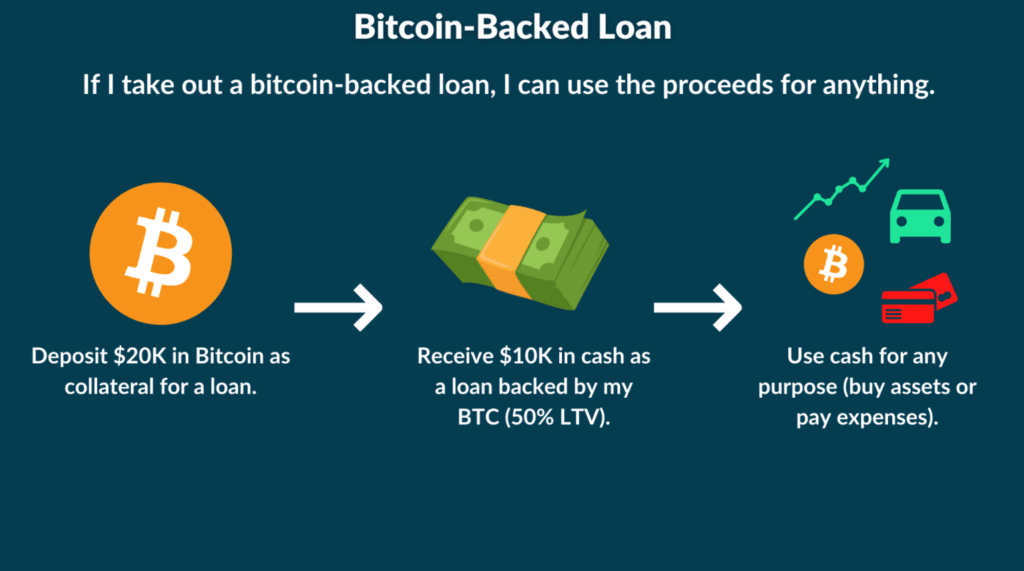

Example: Say an investor takes out a $50,000 personal loan to buy bitcoin @ $50,000, then bitcoin falls 80% to $10,000. As long as the investor continues to make their loan payments, they will keep their bitcoin and can hold it to see if it recovers back to $50,000 and beyond.

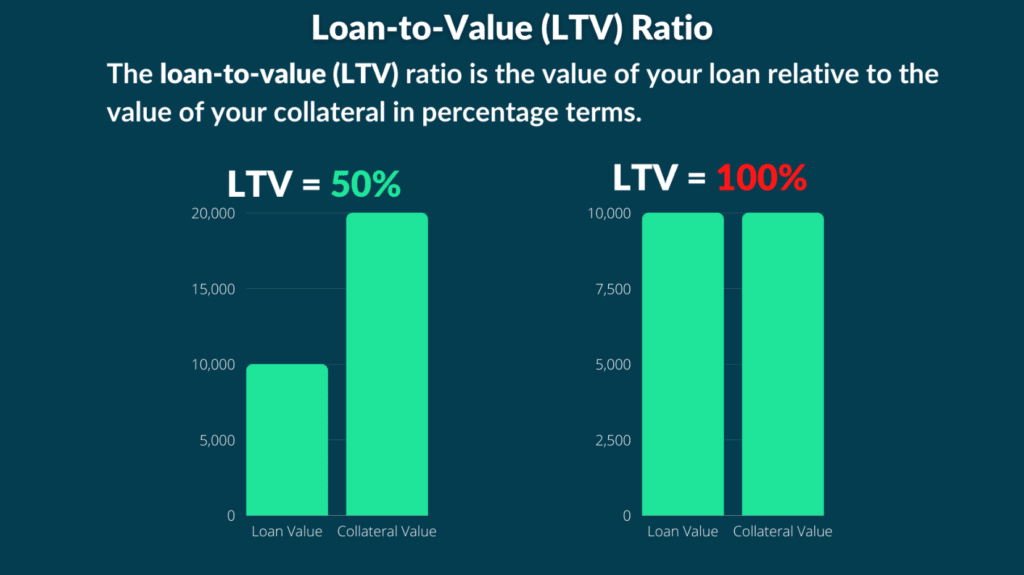

Compare this to an investor who has $100,000 worth of bitcoin and they take out a $50,000 bitcoin-backed loan to buy more bitcoin. Their loan-to-value ratio is 50%.

Then bitcoin falls 50%, cutting the value of their bitcoin position to $50K. Their LTV is now 100% because their loan is $50K and the value of their BTC position is $50K.

In this scenario, the borrower must reduce their LTV by either:

Adding more bitcoin to the collateral account

Paying down some of the loan from other cash sources.

Both options will reduce the value of the loan relative to the collateral.

If they cannot do either, the lender will sell their BTC for $50K to recover the money lent out.

This leaves the investor with $0 in debt and $0 in bitcoin. Full liquidation.

The investor will then deal with the tax consequences and also have zero exposure to bitcoin, which would be tough to stomach if bitcoin’s value surged after liquidation.

It’s reasonable to assume an investor that has amassed $1M in assets would be able to easily afford this payment. If not, there is the option of slowly selling assets to meet the monthly payments, which will reduce the benefits below but will likely still be better than liquidating a huge chunk of the portfolio at the beginning.

Here are the outcomes of the two approaches:

Borrow $250K against a $1M stock portfolio at 3.2% interest for 10 years

Sell $250K of the portfolio

|

The investor who liquidated $250K at the beginning pays a 15% long-term capital gains tax (since I’m assuming accumulating a $1M stock portfolio took decades and most of the value of the portfolio is from capital gains).

To make things simple we’ll just use 15% of the entire $250K generated from the sale. If 50% of the $250K came from capital gains, then the capital gains tax would be $18,250 instead of $37,500. An insignificant difference in this comparison.

By borrowing $250K at 3.2% interest, the investor gets to hold the $1M in stocks for the entire 10-year period. Growing at 8% per year, the portfolio grows to $2,158,925. Total capital gains = $1,158,925. They pay $42,460 in loan interest.

The investor who liquidated $250K of their portfolio at the beginning experienced $869K in capital gains over the 10-year period. Their portfolio ended at $1,619,194.

So the investor who borrowed against their stock portfolio had a $2.16M portfolio vs. a $1.62M portfolio at the end of the 10-year period. The investor that borrowed against their assets to come up with cash experienced nearly $300K more in capital gains over the 10-year period compared to the investor who sold their stocks to come up with cash.

The simple way to interpret this is that investor #1 paid $42,500 in loan interest in exchange for increasing their 10-year capital gains by almost $300,000.

The key consideration here is each investor’s confidence in their ability to make loan payments. As long as the investor in scenario #1 can make the loan payments, they reap the benefits of holding onto their appreciating assets.

A big reason one might want to sell a portion of their assets vs. borrow against their assets is if they are not confident they’ll be able to make the debt payments or do not want any debt.

The point here is that debt isn’t always bad and can be used strategically to improve long-term financial outcomes, which is precisely what the wealthy do.

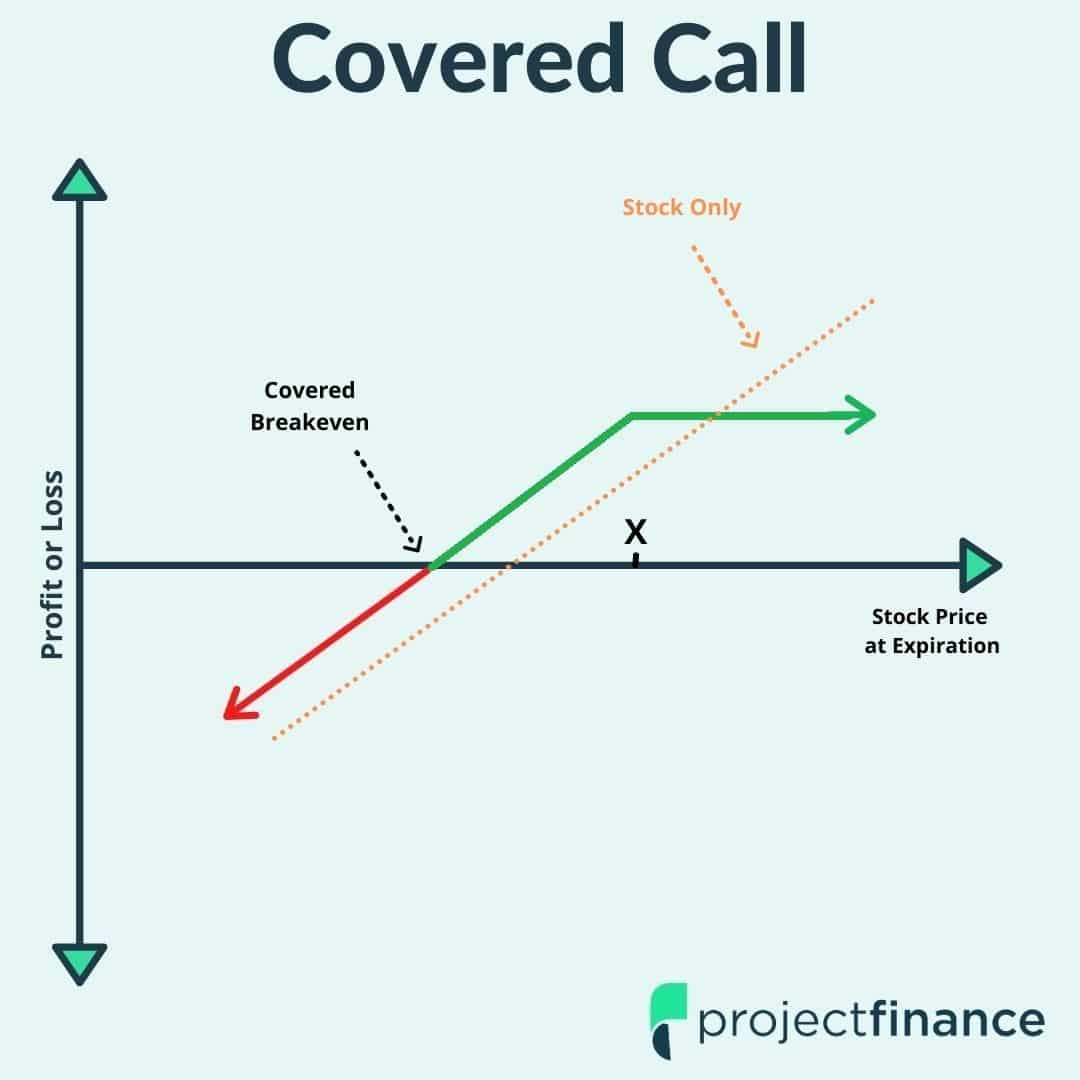

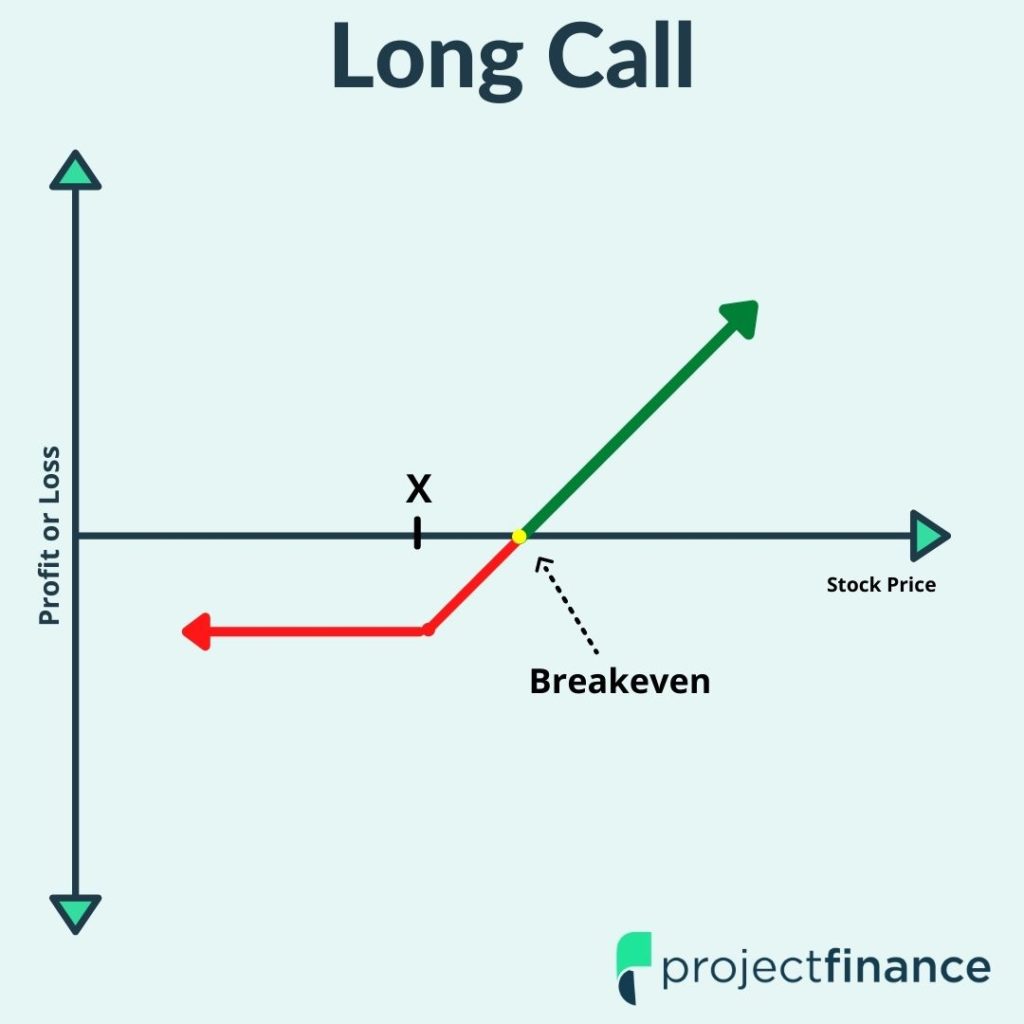

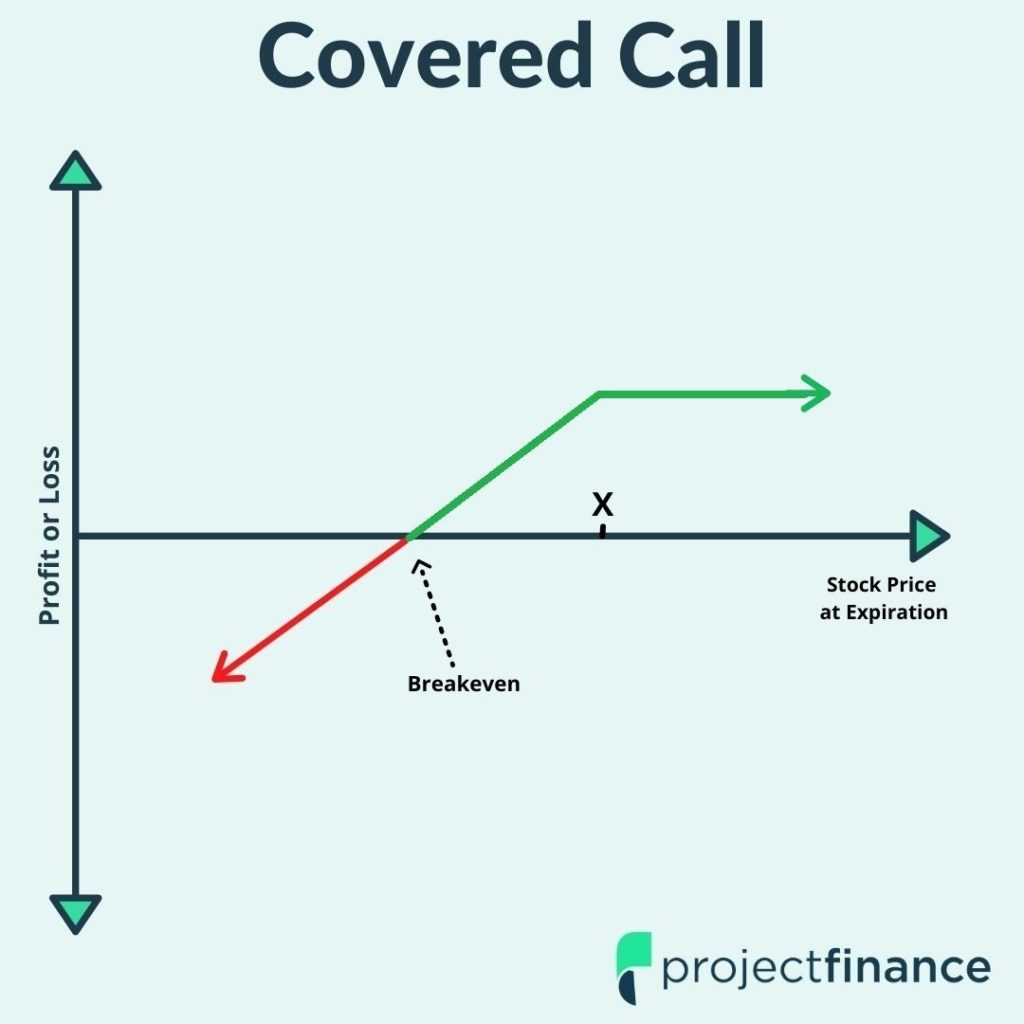

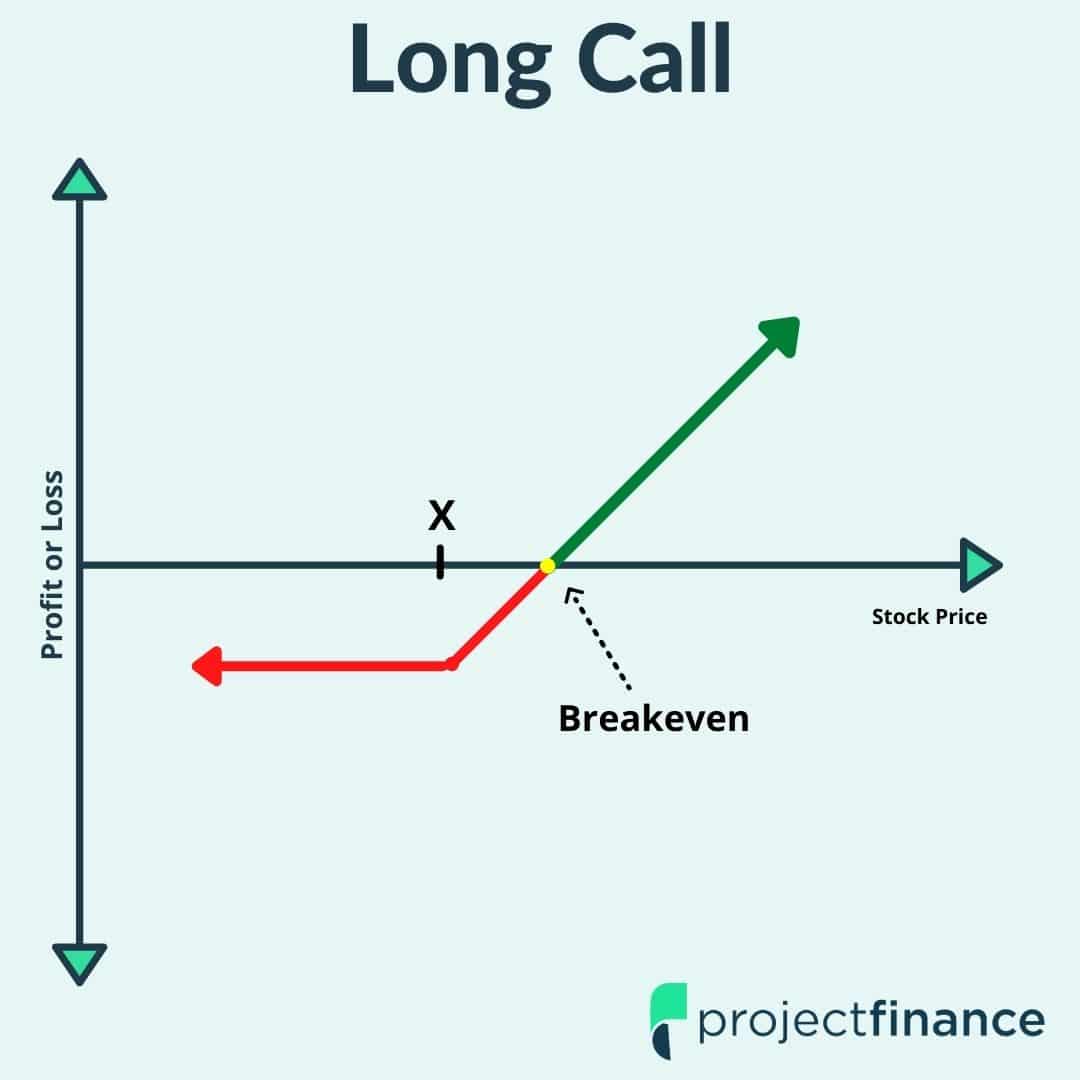

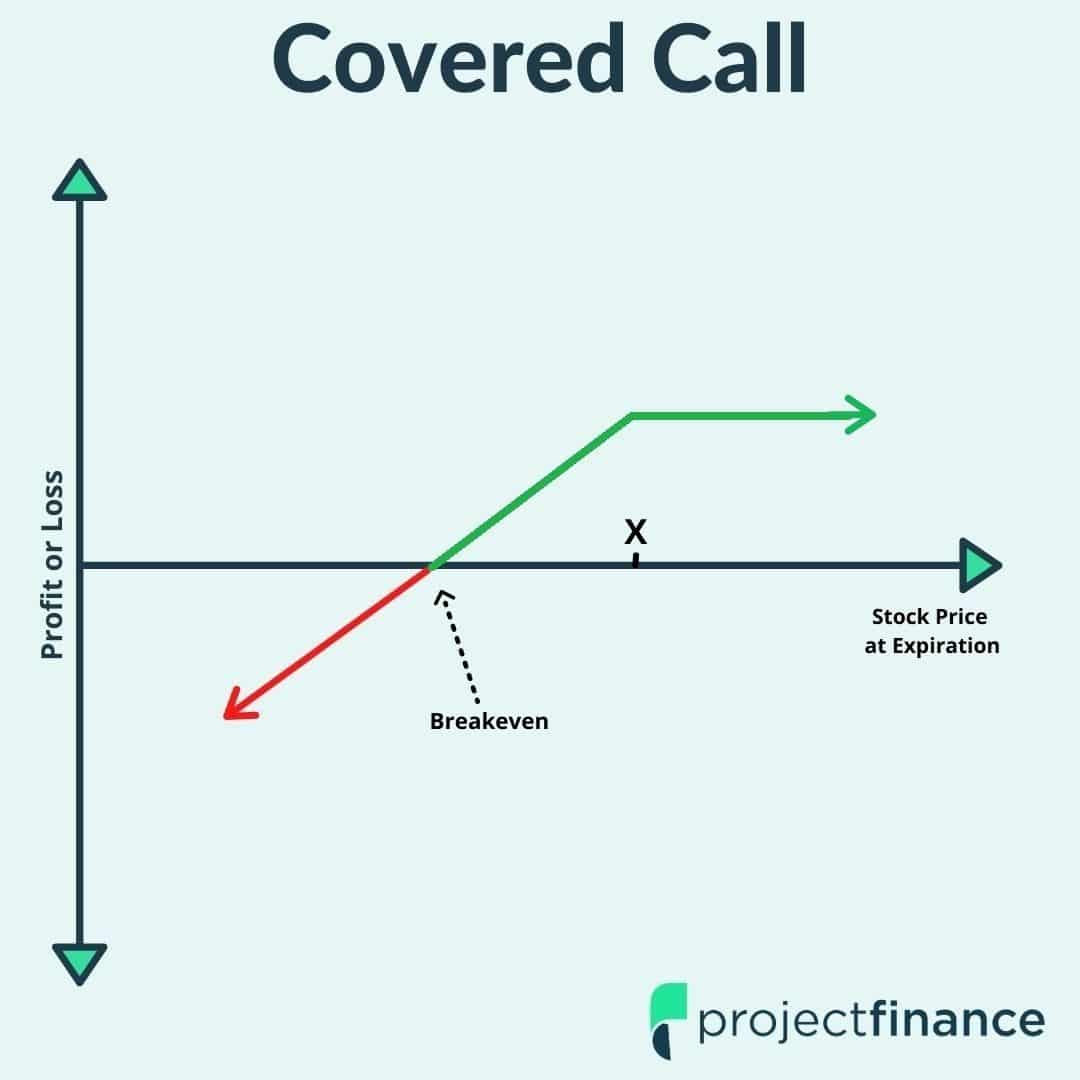

Covered Call vs. Long Call: Here’s How They Differ

Long Call  | Covered Call  | |

When to Trade? | The long call is best suited for traders who are extremely bullish on an underlying security. | The covered call is a great way for investors to collect income on a stock that they believe will change little in the future. |

Maximum Profit Potential | Unlimited (there is no cap on how high a stock can go) | Short Call Strike Price - Stock Entry Price) + Option Premium Collected |

Maximum Loss Potential | Entire Premium Paid | Stock Entry Price - Option Premium Collected |

Breakeven | Strike Price + Premium Paid | Stock Price - Short Call Premium Collected |

Time Decay Effect | As time passes, and both implied volatility and stock price stay the same, a long call option will persistently shed value. | As time passes, and both the implied volatility and stock price stay the same, the short call portion of a covered call will shed value, which is desirable as a short option profits when its value falls. |

Ideal Market Direction | Bullish | |

Tips | In the long run, buying call options is usually a losing battle. For out-of-the-money calls, you need the stock to go up in value - by a lot. Time is NOT on your side here. | The covered call is a great way for all investors to make a little extra money from their stock in a neutral market. Over the long run, however, owning the stock outright is usually more advantageous. |

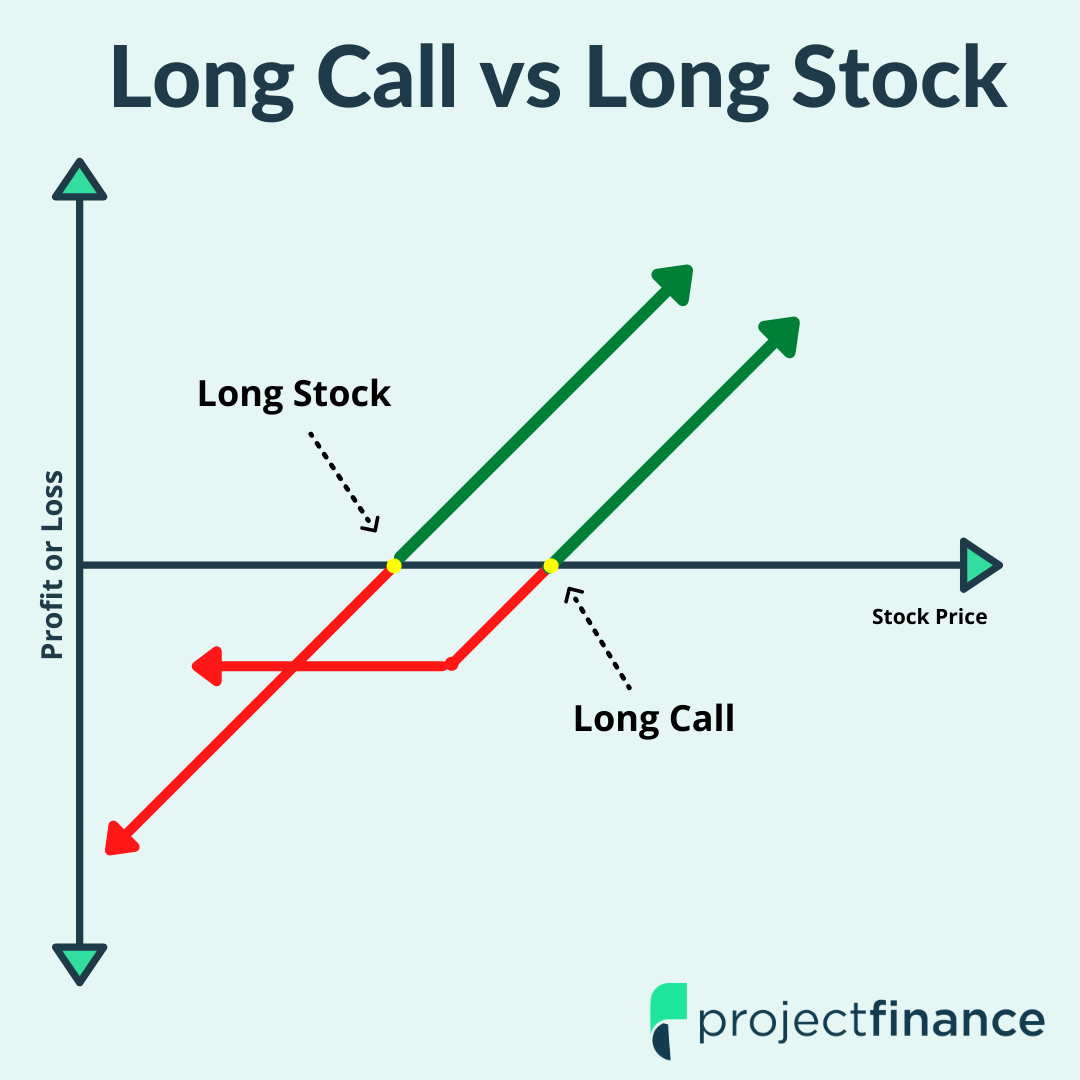

Call Options vs. Shares: 6 MAJOR Differences

SWAR: 2X Leveraged Software ETF Explained

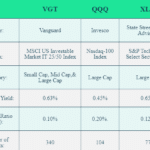

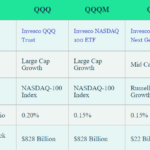

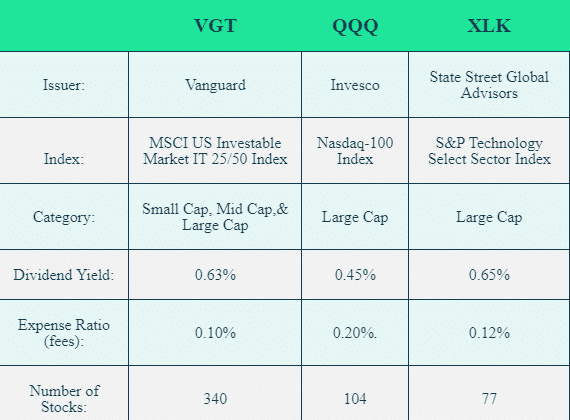

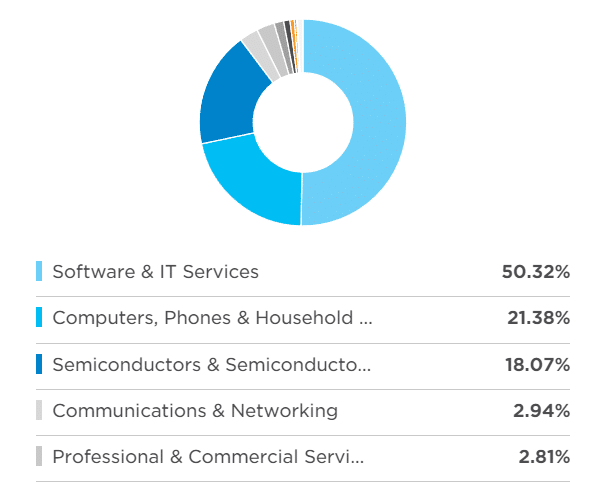

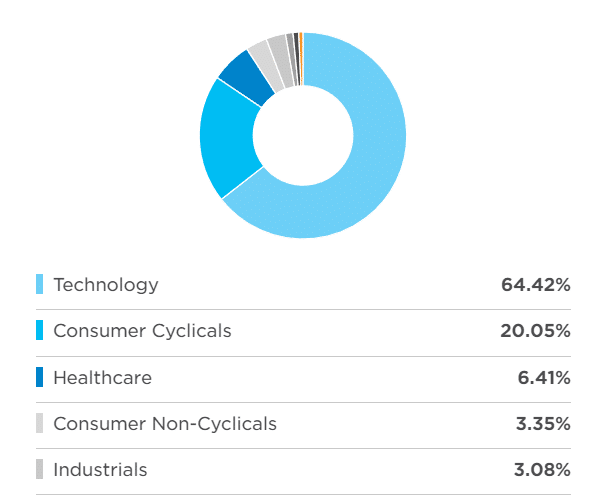

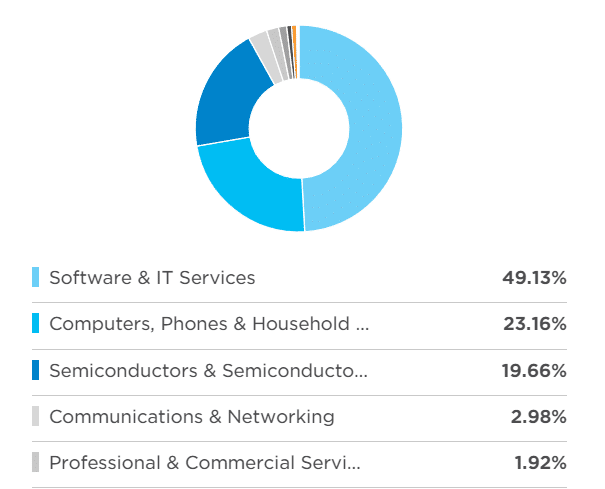

VGT vs QQQ vs XLK: Performance and Holdings

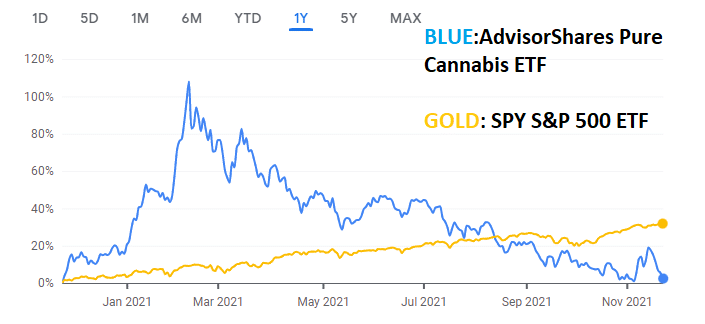

PSDN: AdvisorShares Poseidon Cannabis ETF Explained

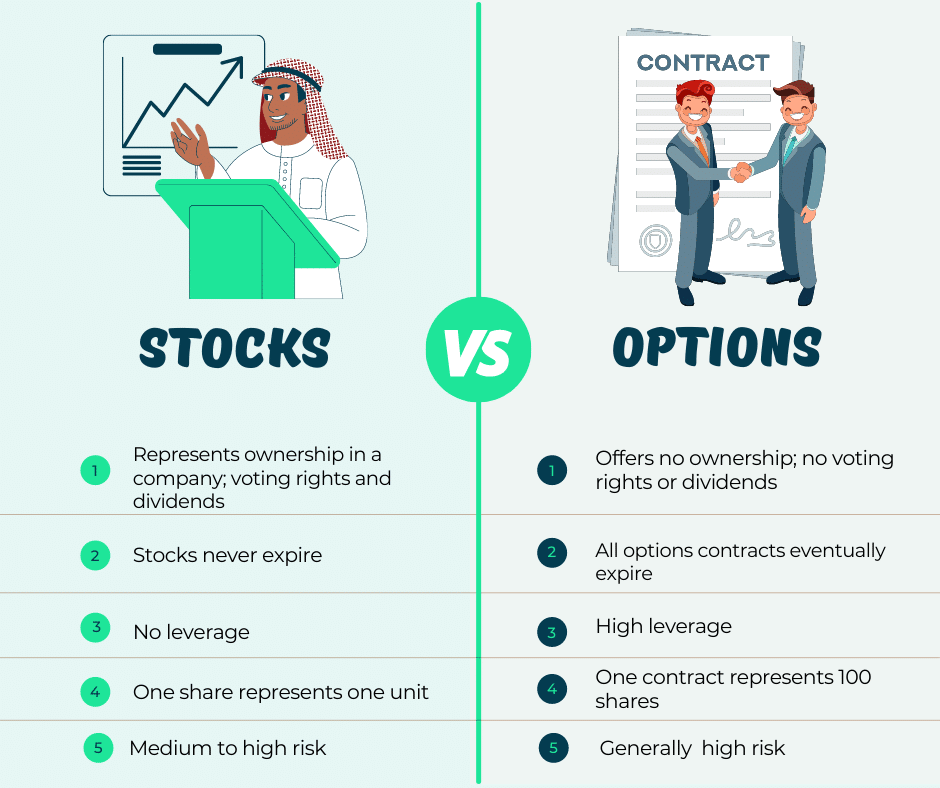

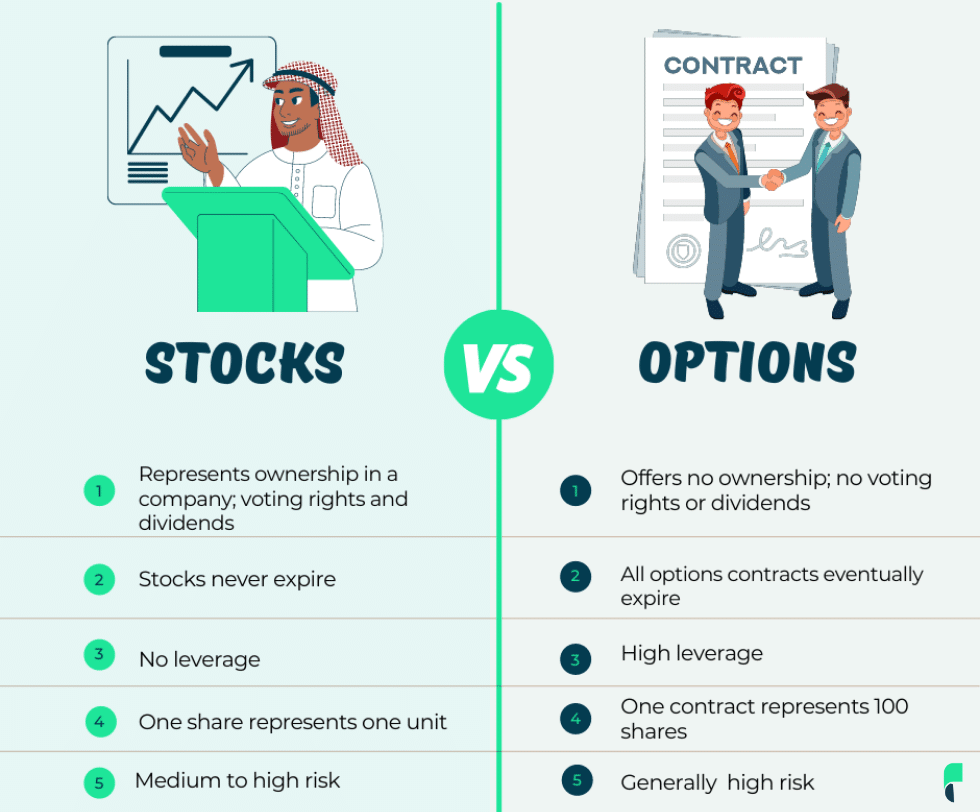

5 Ways Stocks Differ From Options

The Great Resignation, Entrepreneurship and Stocks

ETFs Explained: Investing Basics