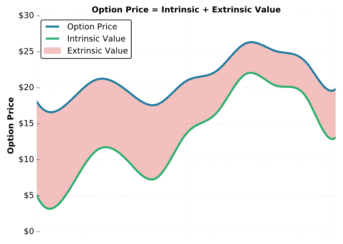

Options Trading Intrinsic & Extrinsic Value Explained (Options Trading) Read More » February 10, 2022

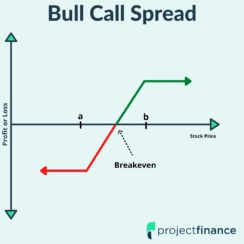

Options Trading Bull Call Spread Explained – The Ultimate Guide w/ Visuals Read More » March 24, 2022