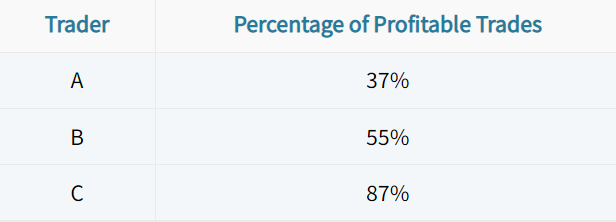

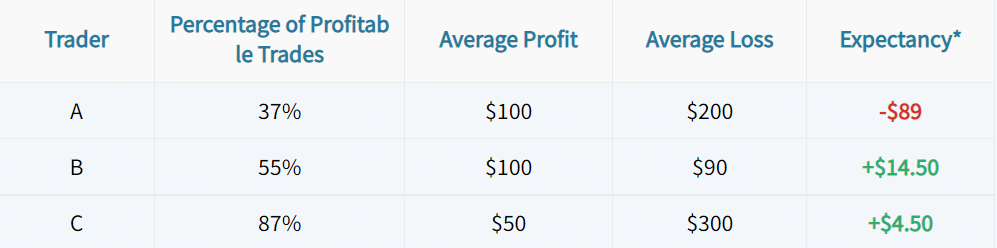

As an illustration, we analyzed the price changes of a call option traded on SPY. Here are the specifics:

Stock: S&P 500 ETF (ticker symbol: SPY)

Time Period: January 29th, 2016 to March 18th, 2016

Option: March 195 Call

Let’s take a look! In particular, pay attention to the relationship between the price changes of SPY and the call option:

As shown here, there is a strong relationship between the price changes of the stock and the call option. A call’s positive delta expresses the direct correlation between the stock price and the call price.

Next, we’ll look at the same example, except we’ll swap out the call option with a put option.

In this example, we’ll visualize the price changes of the March 200 put on SPY.

In particular, note the correlation between the price changes of SPY and the put option.

As illustrated here, the put option’s price is inversely related to changes in the price of SPY shares. A put option’s negative delta expresses the inverse correlation between the stock price and the put’s price.

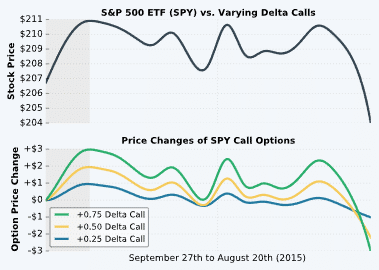

First, let’s start with the setup for this example:

Stock: S&P 500 ETF (ticker symbol: SPY)

Time Period: September 27th, 2015 to August 20th, 2015

Expiration: August 21st, 2015

To visualize the price changes of SPY call options with different deltas, we analyzed three separate call options with deltas of +0.25, +0.50, and +0.75, respectively. When examining this visual, notice how each option’s delta translates to its degree of price sensitivity:

In the highlighted area, SPY experienced a $4 increase in its price. How did each call option’s price respond?

To analyze put option price sensitivity based on the option’s delta, we’ll use the same stock, time period, and expiration cycle as before. However, we’ll analyze three separate SPY put options with deltas of -0.25, -0.50, and -0.75, respectively.

In the highlighted area, SPY experienced a $4 increase in its stock price. How did each put option respond?

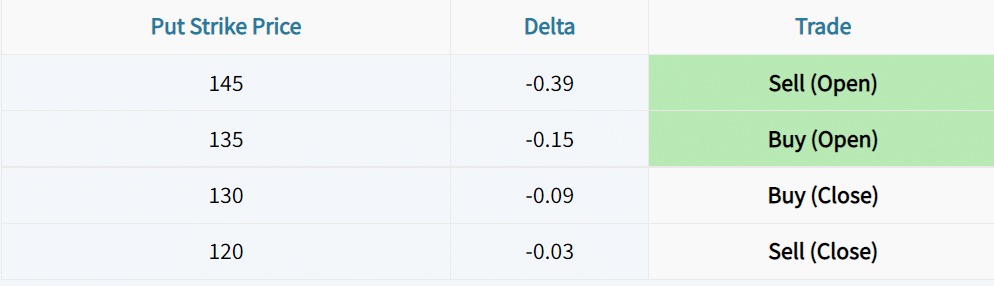

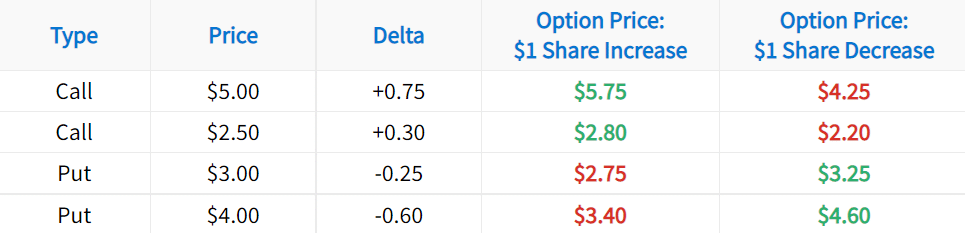

The following visual serves as a visual representation of the table above:

At strike prices lower than the stock price, call deltas are closer to +1, and put deltas are closer to 0. At strike prices near the stock price ($207), option deltas are close to ±0.5. At strike prices above the stock price, call deltas are closer to 0 and put deltas are closer to -1.

As an options trader, you have full control over the strike price you trade.

When trading in-the-money options, you will have more profit/loss exposure when the stock price changes.

When trading out-of-the-money options, you will have less profit/loss exposure when the stock price changes.