Author: Chris Butler

Bearish Options Trading Strategies (In-Depth Tutorials)

The Ultimate Bullish Option Strategy Guides

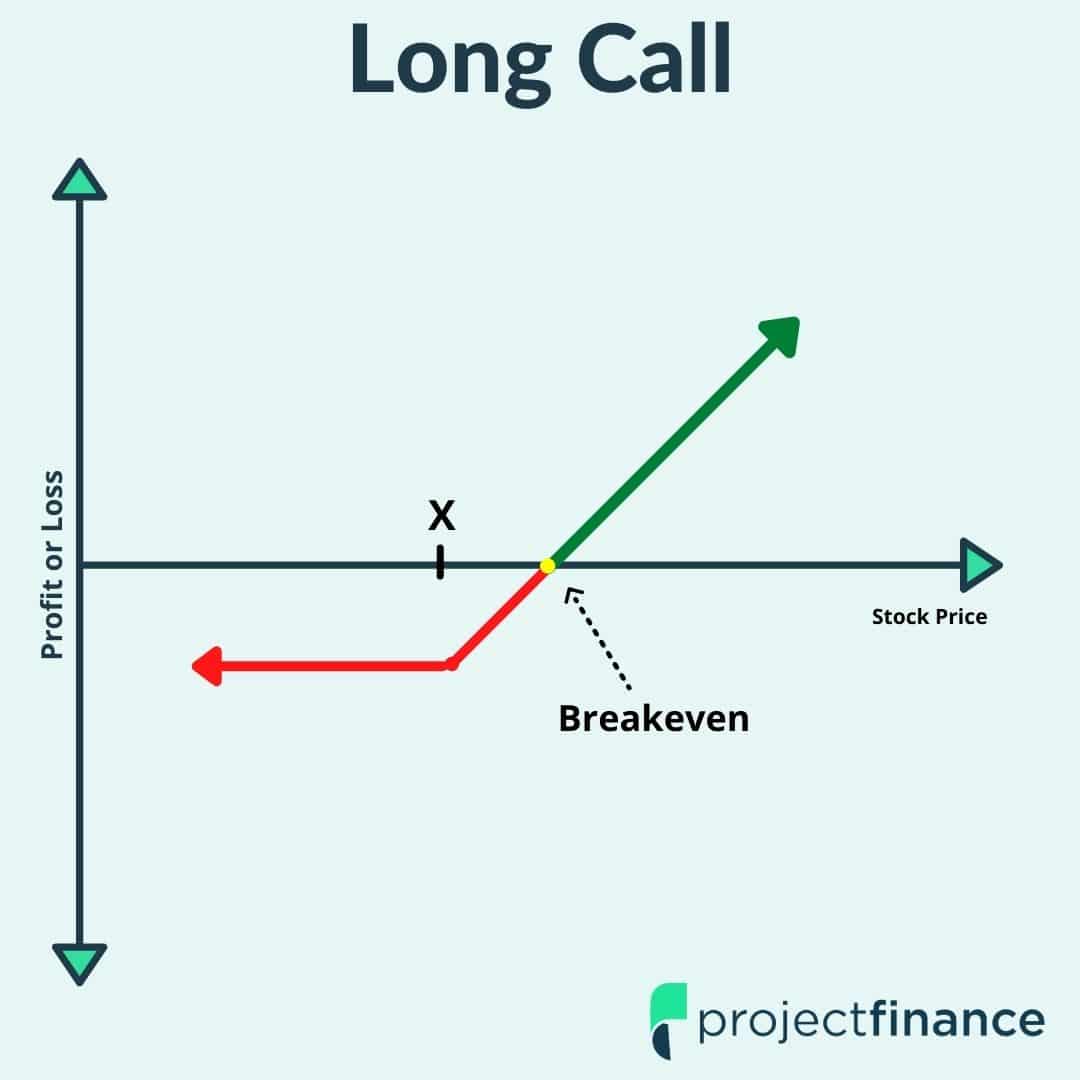

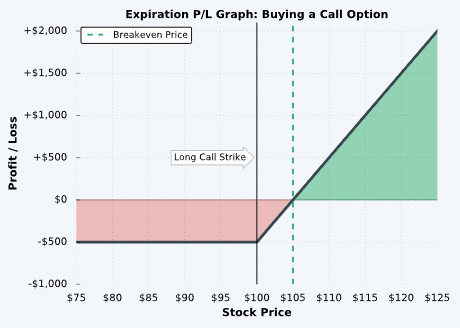

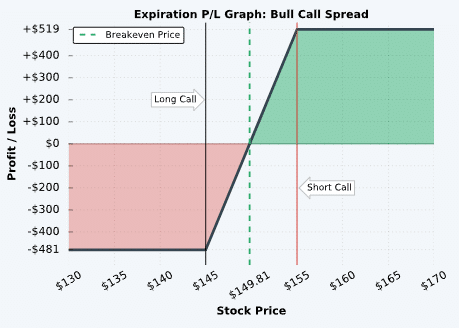

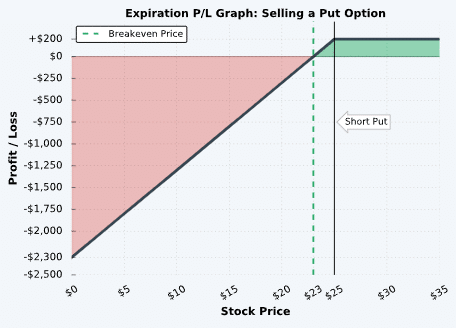

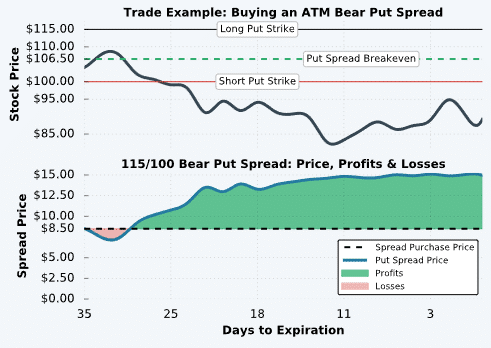

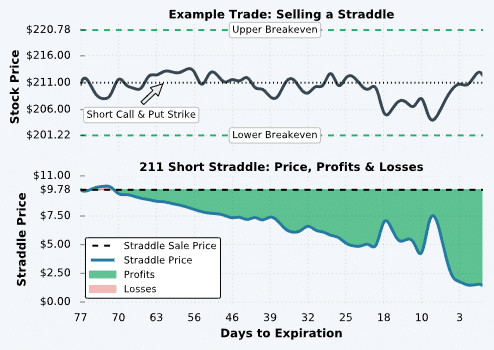

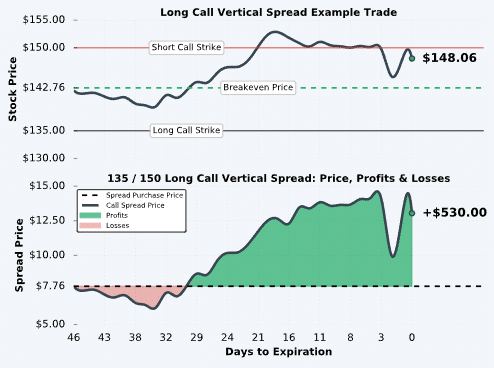

Options Trading Strategy Guides (With Trade Visuals)

tastytrade Analysis Tab (Trading Platform Tutorial)

tastytrade Positions Tab (Trading Platform Tutorial)

tastytrade Trade Tab (Ultimate Trading Platform Tutorial)

Why Trade With tastytrade? (Ultimate Platform Overview)

IV Rank vs. IV Percentile: Which is Better?

Implied volatility rank (IV rank) compares a stock’s current IV to its IV range over a certain time period (typically one year).

Here’s the formula for one-year IV rank:

For example, the IV rank for a 20% IV stock with a one-year IV range between 15% and 35% would be:

An IV rank of 25% means that the difference between the current IV and the low IV is only 25% of the entire IV range over the past year, which means the current IV is closer to the low end of historical volatility.

Furthermore, an IV rank of 0% indicates that the current IV is the very bottom of the one-year range, and an IV rank of 100% indicates that the current IV is at the top of the one-year range.

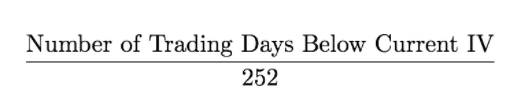

Implied volatility percentile (IV percentile) tells you the percentage of days in the past that a stock’s IV was lower than its current IV.

Here’s the formula for calculating a one-year IV percentile:

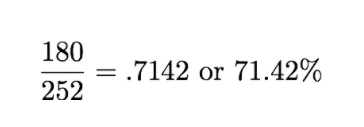

As an example, let’s say a stock’s current IV is 35%, and in 180 of the past 252 days, the stock’s IV has been below 35%. In this case, the stock’s 35% implied volatility represents an IV percentile equal to:

An IV percentile of 71.42% tells us that the stock’s IV has been below 35% approximately 71% of the time over the past year.

VIX Term Structure – The Ultimate Guide w/ Visuals

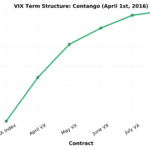

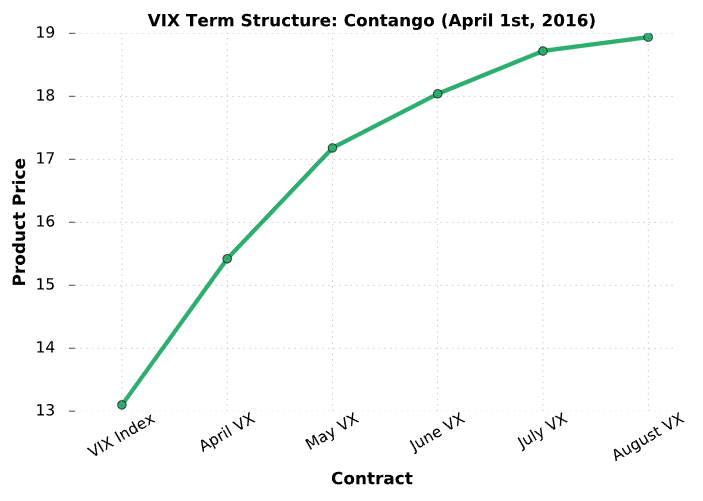

The following chart demonstrates what an upward-sloping (contango) VIX term structure looks like:

Data gathered from the Cboe’s Historical VIX Futures Database

In this example, the VIX Index itself is just above 13 while the August VIX future (approximately 120 days away from settlement) is six points higher at 19. The upward sloping nature of the curve suggests that market participants believe volatility will increase from 13 in the future, which makes sense because the long-term average VIX level is around 20.

In the event that the VIX Index (prices of S&P 500 options) remains around 13, the price of each of these VIX futures contracts will lose value as time passes.

Consequently, any long VIX futures traders will lose money, as well as traders who have on bullish trades in related volatility products (bullish VIX option trades, VXX, UVXY, etc.). On the other hand, traders with short VIX futures contracts or bearish positions in volatility products will are likely to profit (bearish VIX option trades, long XIV or SVXY, etc.).

The following chart demonstrates what a downward-sloping (backwardated) VIX term structure looks like:

Data gathered from the Cboe’s Historical VIX Futures Database

In this case, the VIX Index is above 27. However, the June VIX futures contract (roughly 150 days until settlement) is four points lower at 23. The downward-sloping nature of the curve suggests that market participants believe volatility will decrease from 27 in the future, which makes sense because the long-term average VIX level is around 20.

In the event that the VIX Index (prices of S&P 500 options) remains around 27, the price of each of these VIX futures contracts will “slide up the curve” as time passes. Consequently, any short VIX futures traders will lose money, as well as traders who have on bearish trades in related volatility products (VIX options, VXX, UVXY, etc.). However, any traders who are long VIX futures or have bullish positions in volatility products are likely to make money.d

In the final example, we’ll look at a relatively flat VIX term structure from early 2016:

Data gathered from the Cboe’s Historical VIX Futures Database

In this case, the VIX index is at 20 while the five subsequent VIX futures contracts are near 21. While not exactly equal, this VIX futures curve can be described as flat. When the VIX term structure is flat, long and short volatility trades don’t stand to gain or lose too much money if the VIX remains at its current level of 20. However, this could change quickly if the shape of the curve transitions into steep contango or backwardation.