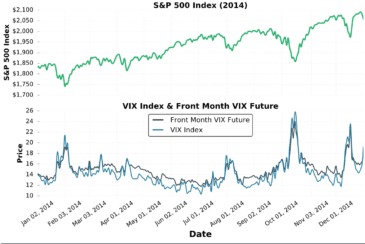

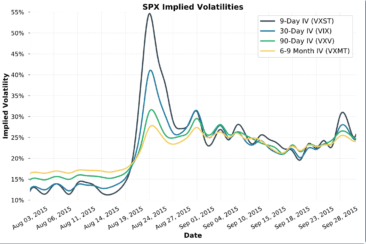

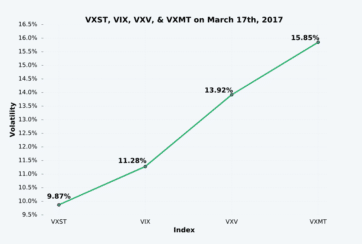

Options Trading How Options Volatility Products Work: VXST, VIX, VXV, VXMT Read More » March 15, 2022

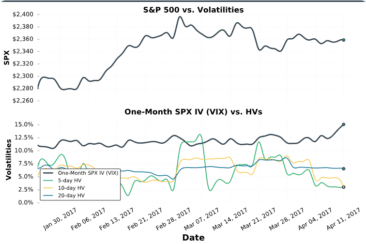

Options Trading Historical Volatility Explained: Is it Useful to Options Traders? Read More » February 10, 2022