Search

About

Blog

Contact

About

Blog

Contact

Search

Watch on YouTube

Author:

Chris Butler

Retirement

How to Calculate Your Roth IRA and 401k Paychecks

Read More »

April 25, 2022

Retirement

FAQ: How Much Cash Should Retirees Keep on Hand?

Read More »

April 14, 2022

Retirement

Can You Contribute to Multiple 401(k) Accounts Simultaneously?

Read More »

April 13, 2022

Investing

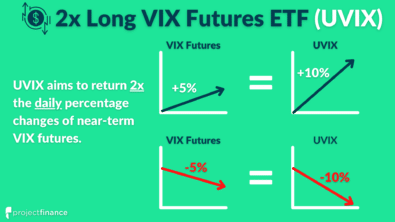

What is UVIX? (2x Long Volatility ETF Explained)

Read More »

March 29, 2022

Investing

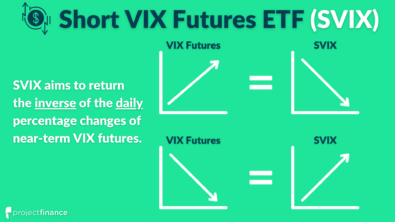

What is SVIX? (Short Volatility ETF Explained)

Read More »

March 29, 2022

Investing

Money 101: The Functions & Characteristics of Money

Read More »

April 25, 2022

Options Trading

Poor Man’s Covered Call [The Ultimate Beginner’s Guide]

Read More »

May 6, 2022

Options Trading

VIX Contango: The Ultimate Beginner’s Guide

Read More »

March 28, 2022

Options Trading

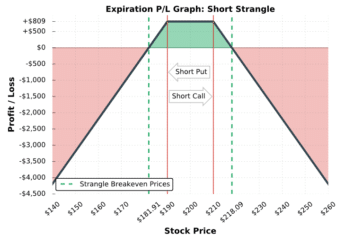

Short Strangle Adjustment: Rolling Up the Short Put

Read More »

March 2, 2022

Options Trading

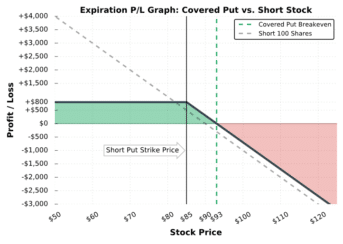

Covered Put Writing Explained (Best Guide w/ Examples)

Read More »

March 25, 2022

«

Page

1

Page

2

Page

3

Page

4

Page

5

»