Search

Search

About

Blog

Contact

Menu

About

Blog

Contact

Search

Search

Watch on YouTube

Month: May 2022

Options Trading

Bid Size vs. Ask Size in Options & Stocks Explained

Read More »

September 15, 2022

Options Trading

29 Core Options Trading Strategies For Beginners

Read More »

May 9, 2022

Options Trading

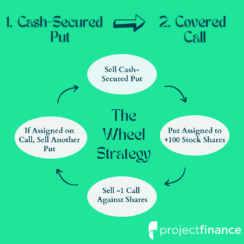

The Wheel Options Strategy: Collect Income From Options

Read More »

May 25, 2022