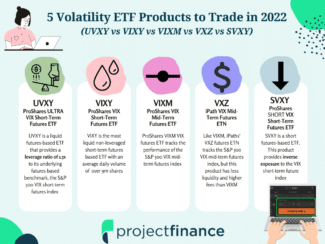

Investing VXX Alternatives: UVXY vs VIXY vs VIXM vs VXZ vs SVXY vs UVIX vs SVUX Read More » April 1, 2022

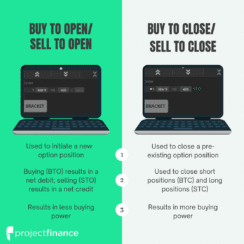

Options Trading Options: Buy to Open vs Buy to Close & Sell to Open vs Sell to Close Read More » May 4, 2022