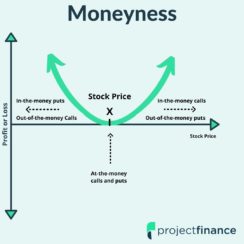

Options Trading Option Moneyness: In The Money, At The Money and Out Of The Money Read More » March 17, 2022